Is 650 a Good Credit Score?

The short answer is no — but it's not bad either. A 650 credit score is a fair score. It sits below the U.S. average and just under the "good" tier, which means you can usually get approved for credit, but you'll pay more for it than someone a few points higher.

That gap matters more than most people realize. The difference between a 650 and a 720 isn't a letter grade on a report card — it's tens of thousands of dollars over the life of your loans, the difference between a 6.5% mortgage and an 8% one, between a 4.66% car loan and a double-digit one.

So if you're sitting at 650 right now, here's the honest framing: you're not in trouble, but you are leaving real money on the table. The good news is that 650 is one of the easiest scores to improve quickly, because you're already so close to the next tier. Let me walk you through exactly what a 650 means, what it gets you, what it costs you, and how to push past it.

Where 650 Actually Falls on the Scale

There are two scoring systems that matter in the U.S.: FICO and VantageScore. Both run on a 300–850 scale, and on both, a 650 lands in the fair range.

FICO — used by roughly 90% of top U.S. lenders — breaks the scale into five tiers:

| FICO Tier | Score Range | Where 650 Lands |

|---|---|---|

| Poor | 300–579 | |

| Fair | 580–669 | ← You are here |

| Good | 670–739 | |

| Very Good | 740–799 | |

| Exceptional | 800–850 |

VantageScore uses the same 300–850 scale and also classifies 650 as fair. Capital One confirms that both FICO and VantageScore treat 650 as a fair score — so no matter which model a lender pulls, the verdict is the same.

The single most important number to remember: the "good" range starts at 670. You are only 20 points away from changing tiers. In credit terms, that's nothing — a couple of months of the right moves can cover that distance.

Is 650 Below Average?

Yes. As of 2025, the average U.S. credit score is around 715, according to Experian. Consumer Reports notes that, as of August 2025, the average score across all auto-loan borrowers was 715 — with new-car buyers averaging 757 and used-car buyers 690.

A few statistics from Experian put a 650 in perspective:

- 76% of U.S. consumers have a score higher than 650. You're in the lower quarter of the country — but climbing out of it is straightforward.

- 17% of all consumers sit in the fair range (580–669) alongside you, per Experian.

- Lenders often label this range "subprime" or "nonprime," which is shorthand for "slightly higher risk." Experian's data shows that about 28% of consumers in the fair range go on to become seriously delinquent — which is exactly why lenders price the risk into your rate.

None of this means you're stuck. It means the system currently sees you as an unknown quantity, and your job is to give it more reasons to trust you.

What a 650 Usually Says About Your File

Everyone arrives at 650 by a different path, but the patterns are remarkably consistent. According to Experian, among Americans sitting right at a 650:

- 72% have at least one payment that was 30+ days late. Payment history is the single biggest factor in your score, so even one slip drags you down.

- The average credit utilization rate is 47.9%. That's wildly high. Lenders want to see you using a small fraction of your available credit, not nearly half of it.

- The average credit card balance is $6,554. High balances and high utilization usually travel together.

If you recognize yourself in that list, you've also just found your roadmap. The two biggest drags on a fair score — late payments and high utilization — are also the two fastest levers you can pull. We'll get to the exact mechanics below.

What You Can Actually Get With a 650

This is the question that matters most. A score is only meaningful in terms of what it unlocks. The honest summary: at 650 you can get approved for almost every category of credit, but you're locked out of the best terms within each one. Here's the at-a-glance version, followed by the detail that matters.

| Product | What a 650 Can Get | What a 650 Can't Get (Yet) |

|---|---|---|

| Credit cards | Secured cards, starter cards, store cards, some fair-credit unsecured and cash-back cards | Premium travel/rewards cards (usually 680+), the highest limits, the lowest APRs, top 0% balance-transfer offers |

| Auto loans | Approval at nonprime rates on new and used cars | Prime and super-prime APRs (the cheap money) |

| Mortgages | FHA, VA, USDA, and conventional loans (you clear every program minimum) | Jumbo loans (usually 700–720+), the best rates, freedom from lender "overlays" |

| Personal loans | Approval from fair-credit and many mainstream lenders | The lowest APRs; some prime-only lenders will pass, and origination fees are common |

| Renting & insurance | Approval in most cases | Waived deposits, the lowest insurance premiums, the strictest 700+ buildings |

Credit Cards

A 650 will get you approved for plenty of cards — just not the premium ones. You'll qualify for secured cards, starter cards, store/retail cards, and a number of unsecured cards aimed at fair credit. According to WalletHub, real options at this level include no-annual-fee starter cards and flat-rate cash-back cards, and you can even land an entry-level business card. Some unsecured fair-credit cards carry APRs in the rough range of 25%–36%, so the rate deserves close attention before you treat any of them as a spending card.

What you typically won't get yet: the top travel cards, the biggest sign-up bonuses, the highest limits, the lowest APRs, or most 0% intro balance-transfer offers — those are generally reserved for scores of 680 and up. Expect a modest starting limit and an above-average interest rate.

The smart play at 650 is to use a card lightly, pay it in full before the statement closes, and let the clean history do the work. Many issuers automatically review you for a limit increase — or graduation from a secured to an unsecured card — after six to eight months of on-time payments, which is exactly the kind of momentum that carries you toward 700.

Auto Loans

This is where a 650 costs you in cash you can feel. Lenders tier auto rates aggressively by score. Using Experian's State of the Automotive Finance Market data, here's roughly how the tiers shake out:

| Credit Tier | Score Range | Avg. New-Car APR | Avg. Used-Car APR |

|---|---|---|---|

| Super Prime | 781–850 | ~4.7% | ~6.8% |

| Prime | 661–780 | ~6.7% | ~9.5% |

| Nonprime | 601–660 | ~9.8% | ~14.1% |

| Subprime | 501–600 | ~13.3% | ~19.0% |

| Deep Subprime | 300–500 | ~16.0% | ~21.6% |

Rates are illustrative averages based on Experian Q3–Q4 2025 data via Self and U.S. News; your actual rate will vary by lender, term, and down payment.

Look at the jump. A 650 sits at the bottom of the nonprime tier, so on a new car you're looking at roughly 9.8% versus the ~6.7% a prime borrower gets — and versus the 4.7% a super-prime borrower gets. On a $35,000, 60-month loan, that spread between nonprime and super-prime is well over $5,000 in extra interest for the exact same car.

Mortgages

A 650 will not lock you out of homeownership. In fact, it clears the program minimum for every major loan type. What changes is the rate you're offered and how much scrutiny the rest of your file gets.

Here are the typical credit-score minimums for each program, per LendingTree and UQUAL:

| Loan Type | Typical Minimum Score | Does a 650 Qualify? |

|---|---|---|

| FHA (3.5% down) | 580 | ✅ Yes, comfortably |

| FHA (10% down) | 500 | ✅ Yes |

| VA | No federal minimum; lenders want ~620 | ✅ Usually |

| USDA | ~640 | ✅ Yes |

| Conventional (Fannie/Freddie) | 620 | ✅ Yes |

| Jumbo | 700–720+ | ❌ Not yet |

So at 650 you qualify for FHA, VA, USDA, and conventional financing — you only miss jumbo loans, which need stronger profiles because they exceed conforming limits. You're not alone here either: Equifax data cited by WalletHub shows that roughly 17% of first mortgages go to borrowers scoring below 660.

Two important caveats. First, lender overlays: program minimums are the floor, but individual lenders often add their own requirements 20–40 points higher, so a 650 won't be welcomed everywhere. Second, rate. In the current market a 650 borrower is looking at conventional rates roughly in the 6.5%–8.5% range and FHA/VA around 6%–7.5%; Better estimates a typical 650 mortgage rate around 7.4%. For context, the average conventional borrower in 2024 had a 755 score, and the best pricing is reserved for that tier.

To put the rate gap in real numbers — the same example from our 800 credit score guide — on a $400,000, 30-year mortgage, a borrower near 760 might lock 6.5% while a 620 borrower gets closer to 8%. That single difference works out to roughly $425,000 in extra interest over the life of the loan for the identical house. A 650 sits between those two points, but the lesson holds: a few tiers of score improvement before you apply can save you a fortune.

Personal Loans

You can get a personal loan at 650, but you'll be quoted higher APRs and lower limits than prime borrowers, and some of the best online lenders will pass. WalletHub notes that most personal loans require a score of at least 660, so a 650 narrows your menu and almost any loan you do land is likely to carry an origination fee. Lenders that specialize in fair-credit borrowers exist — they just price the risk in. If your goal is debt consolidation, run the math carefully: a high-APR consolidation loan can cost more than the debt you're trying to escape.

Student Loans, Renting, and Insurance

A couple of bright spots and a couple of hidden costs round out the picture. Student loans are among the easiest to get at 650 — federal student loans don't use credit scores at all. On the flip side, credit follows you well beyond loans: landlords pull credit before approving a lease (and, as I learned the hard way, many premium buildings want 700+), auto insurers in most states use a credit-based insurance score to set premiums, and utility or phone companies may ask for a deposit. None of these are dealbreakers at 650, but each is a place where a higher score quietly saves you money or skips a deposit.

The Real Cost of Staying at 650

Here's the part nobody puts on a credit report. A 650 doesn't just cost you on one loan — it taxes everything you finance, at the same time, for years.

Think about a typical household over a decade: a car loan or two, a mortgage, a few credit cards, maybe a personal loan. At 650, every one of those carries a "fair credit" surcharge baked into the rate. Add it up and the lifetime cost of sitting in the fair range instead of the good-to-very-good range routinely runs into the tens of thousands of dollars.

That's the math that should motivate you. You're not improving your score to win a game. You're doing it because the gap between 650 and 720 is, in dollar terms, one of the highest-return moves available to an ordinary household — and it requires no extra income, just better mechanics.

Why a 650 Is Actually Good News

I want to reframe this, because the doom-and-gloom around fair credit misses the point.

A 650 is the easiest scoring position to improve from. You're 20 points from "good" and not far from "very good." You almost certainly aren't dealing with a bankruptcy or foreclosure (those push scores far lower). In most cases, a 650 is the result of two fixable things: a late payment or two, and high utilization. Both respond fast to the right actions — sometimes within a single billing cycle.

Compare that to someone rebuilding from a 520 after a major derogatory mark. They're looking at years. You're looking at months. That's a genuinely strong position. Let's use it.

How to Move From 650 to 700+

This is the same playbook I used to go from no credit history at all to an 800+ score, condensed to the moves that matter most when you're starting at a fair score. None of this requires carrying debt or paying interest.

1. Crush Your Utilization First

This is your highest-leverage move at 650, because the average person at this score is running 47.9% utilization — and utilization is about 30% of your FICO score.

The standard advice is to stay under 30%. That's the floor, not the goal. Aim for 1–10%. And here's the detail most people miss: your card issuer reports your balance to the bureaus when your statement closes, not when your payment is due. So pay your balance down before the statement closing date, not just before the due date. That way the bureaus see a tiny balance, not the full month of spending.

Do this one thing and you can see movement in 30–60 days. Experian confirms that paying down balances is one of the fastest ways to raise a score.

2. Lock Down Payment History

Payment history is 35% of your FICO score — the biggest single factor. Since 72% of people at 650 have a late payment on file, this is likely part of your story.

You can't undo past lates, but you can stop new ones cold:

- Set up autopay for at least the minimum on every account as a failsafe.

- Then manually pay the full balance before the statement closes to protect utilization.

- Keep going. A single 30-day late can cost 50–100+ points and stays on your report for seven years, so the most valuable payment is the one you don't miss.

3. Report Your Rent and Bills

This is the move almost nobody at 650 is using, and it's tailor-made for fair-credit profiles. You're already paying rent, electric, gas, water, and your phone bill every month — but historically none of it counted toward your credit.

That's changed. Arcane Credit links your bank account through Plaid, automatically identifies your recurring rent and utility payments, and reports them to the bureaus every month — no landlord approval, no paperwork. It's $3.99/mo on the yearly plan, with no hard pull to sign up. You can download Arcane Credit on the App Store and start reporting in minutes.

The data behind this is hard to ignore. A 2021 TransUnion analysis found that adding rental payments to credit reports raised scores by an average of nearly 60 points. And VantageScore states that adding rental data to an established file can add up to 150 points.

If you've been renting for years, Arcane Credit's Score Boost can retroactively report up to 24 months of past payments — so instead of a thin recent history, the bureaus suddenly see two full years of on-time payments backdated into your file. For someone sitting at 650 because of a thin or spotty history, that's one of the most asymmetric moves available.

4. Fix Your Credit Mix

Lenders like to see you handle more than one type of credit — revolving (credit cards) and installment (loans). If your file is all credit cards or all loans, you're leaving points on the table. The painless way to add an installment tradeline is a credit-builder account: you make small monthly payments that are reported as an installment loan, then get the money back at the end. Look for one from an FDIC-insured bank that reports to all three bureaus. Experian explains how credit-builder loans work here.

5. Dispute Errors on Your Report

Before you assume your 650 is "earned," check that it's accurate. A Consumer Reports investigation found that more than a third of people spotted at least one error on their credit report. A single incorrect late payment or collection can suppress your score by 20+ points. Pull your report, and dispute anything wrong directly with Experian, Equifax, or TransUnion. Arcane Credit gives you 24/7 access to your VantageScore and report through the iOS app so you catch problems early instead of after they've cost you a loan.

My Own Climb: From Invisible to the 700s

When I first arrived in the U.S., my score wasn't low — it was nothing. Blank. I was credit invisible, which means that when a company ran my SSN, the bureaus returned nothing at all. In a lot of cases the response wasn't even "low score" — it was identity cannot be found.

That is a strange and frustrating place to be. I couldn't get approved for a T-Mobile SIM card. Most providers couldn't approve me for anything, because as far as the system was concerned, I didn't exist. That part — being a real person with income who the system simply can't see — was the hardest stretch of the whole journey.

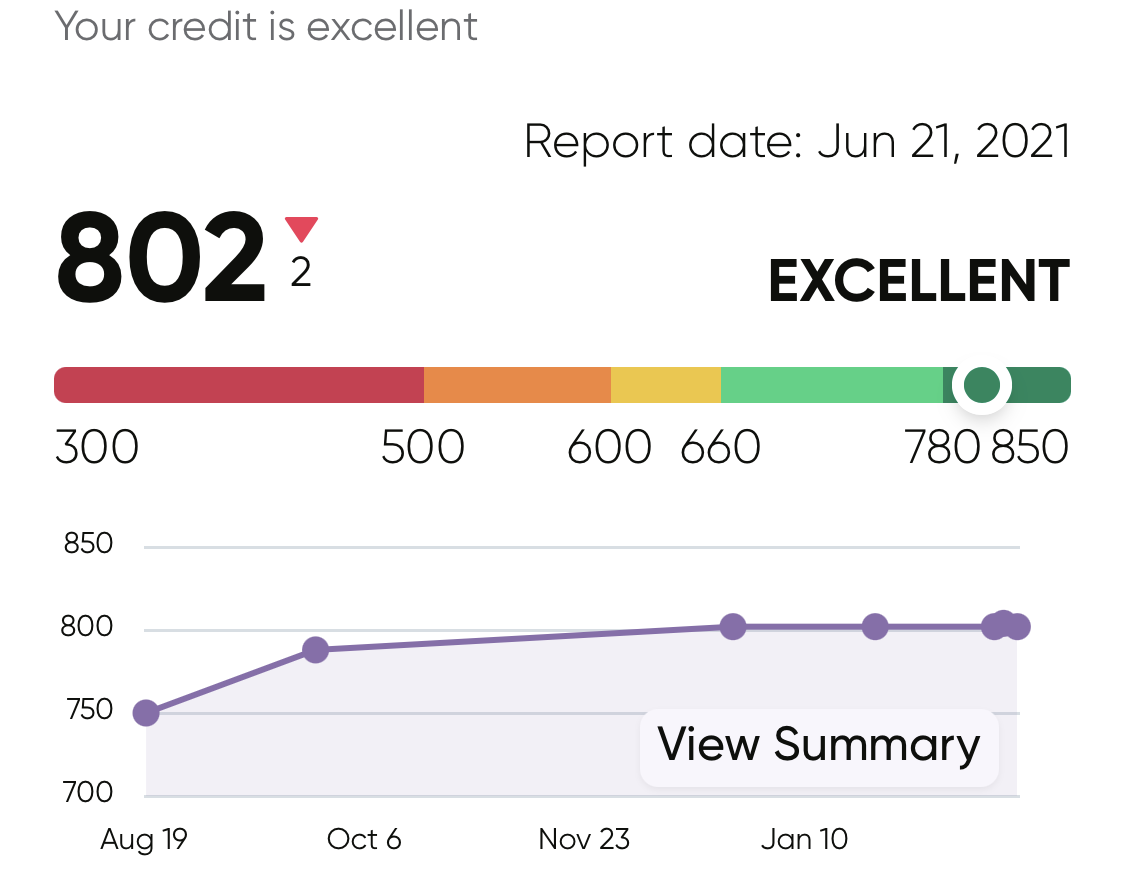

Rent and bill reporting is what broke the logjam. I started reporting the rent and utilities I was already paying every month, and by the second month, my file finally had something in it. My score kickstarted at 650.

That 650 changed my day-to-day immediately. The blank "we can't verify your identity" rejections mostly stopped, and I could get a SIM card. But it also taught me exactly how much credit matters even when money isn't the problem. I was trying to rent a nice house in the Las Vegas suburbs, and landlords there wanted a 700+ score — even though I had more than enough for the security deposit and then some. The cash wasn't the issue. The number was the gate. That's when it really sank in: a fair score isn't neutral, it quietly decides what you're allowed to do.

So I doubled down. I combined month-to-month rent and bill reporting with a one-time back-report of 24 months of past payments — essentially backdating two full years of on-time history into my file — all through the Arcane Credit app. Within about three months, my score climbed into the early 700s.

But here's the lesson that took me longest to learn, and it's the one I want you to walk away with: the three-digit score is only the entry ticket. Once I was actually applying for things, I realized lenders weren't just reading my number — they were reading my whole file. How old was my credit history? Did I have a real mix of credit, or just one type? Had I shown enough experience actually managing accounts over time? Early on, my score said "fair-to-good," but my file was thin and young, and that combination got me second-guessed more than once. The score opens the conversation. The depth of your file is what closes it.

That's the whole point of this section. A fair score isn't a verdict. It's a starting line — and the work you're already doing, paying rent and paying bills, can carry you across it faster than you'd think. Just don't stop at the number.

Your Score Is Only Half the Story

This is the part that almost no "is 650 good?" article tells you, and it's the single biggest reason two people with identical 650 scores can get completely different answers from the same lender.

Your credit score is a summary. When a lender runs a meaningful application — a mortgage, a car loan, a higher-limit card — they pull the full report behind that number and weigh several things the score alone doesn't capture. Old National Bank and Bankrate lay out what underwriters actually look at:

- Age of your credit history. A longer track record gives a lender more data to trust. A 650 built on ten years of accounts reads very differently from a 650 built on eight months. This is why a thin file — few accounts, short history — can get you second-guessed even at a decent score: there simply isn't enough information for the lender to feel confident.

- Credit mix and experience. Lenders want to see that you've handled different types of credit — revolving (credit cards) and installment (auto, personal, or credit-builder loans). A balanced mix demonstrates experience. An all-credit-card file, or a file with a single account, gives them less to go on.

- Debt-to-income ratio (DTI). This is huge and the score ignores it entirely. DTI is your total monthly debt payments divided by your gross monthly income. Even with a strong score, a high DTI signals you may not have room for another payment. A low DTI can rescue a fair score.

- Credit utilization right now. Beyond its effect on the score, lenders read your current balances directly. Consistently maxed cards signal strain even if your score hasn't fully reflected it yet.

- Recent inquiries and new accounts. A flurry of recent applications can look like you're "credit hungry" or facing a cash crunch — a caution flag even if you haven't taken on new debt.

- Income and employment stability. Above all, lenders want evidence you can and will repay. Steady income and employment history can offset a middling score; instability can sink an otherwise fine one.

The practical takeaway: don't obsess over the number in isolation. The same moves that raise a 650 — paying down balances, never missing a payment, adding rent and an installment tradeline, keeping old accounts open — also thicken and age your file and improve your mix and DTI at the same time. You're not just chasing points; you're building a profile a lender can say yes to with confidence. That's the difference between a 650 that gets approved and a 650 that gets declined.

Mistakes That Keep You Stuck at 650

If you've been hovering at 650 for a while, one of these is usually why:

- Carrying a balance to "build credit." This is the most expensive myth in personal finance. You do not need to carry debt or pay interest to build credit — paying in full every month works just as well. Experian confirms it.

- Paying on the due date instead of before the statement closes. By the due date, your high balance has already been reported. Pay early.

- Closing old cards. Closing an account erases its limit (raising your utilization) and eventually shortens your average account age. Keep old accounts open.

- Never reporting rent and utilities. You're making the payments anyway. Not reporting them is free credit-building you're throwing away every month.

- Only checking your score after a denial. Monitor it continuously so you can react to drops and errors before they cost you.

The Bottom Line

So, is 650 a good credit score? No — it's a fair one, sitting below the national average of around 715 and just shy of the "good" range that begins at 670. It'll get you approved for most things, but at a "fair credit tax" you feel on every loan.

But 650 is also one of the best places to start. You're 20 points from a better tier and not far from the rates that save real money. Pull your utilization down, never miss a payment, report the rent and bills you're already paying, add an installment tradeline, and clean up any errors — and a move from 650 into the 700s is a realistic outcome within months, not years.

You're already doing the hard part: paying your bills. The next step is making all of it count. You can download Arcane Credit on the App Store to start turning those payments into credit history today.

Disclaimer: Nothing in this article constitutes a guarantee of credit improvement. Every individual's financial situation is different, and the strategies, techniques, or examples discussed may not apply to everyone. Arcane Credit does not guarantee any increase in your credit score. Results may vary and can be influenced by multiple factors, including your activity with other creditors. Arcane Credit does not remove accurate negative information from credit reports.

FAQs

Is 650 a good credit score to buy a house? It's workable, not ideal. A 650 clears the minimums for FHA loans (580+) and conventional loans (620+), so you can qualify — but you'll pay a higher rate than a 700+ borrower. If you have a few months before applying, raising your score first can save tens of thousands over the life of the mortgage.

Is 650 a good credit score to buy a car? You'll get approved, but at nonprime rates — roughly 9.8% on a new car and 14.1% on a used one, versus around 6.7% and 9.5% for prime borrowers, based on Experian data. Even a small score bump before financing can drop your rate a full tier.

How long does it take to go from 650 to 700? It depends on what's holding you back, but because 650 is usually driven by high utilization and a late payment or two — both fast to fix — many people see meaningful movement within one to three billing cycles. Paying balances down before the statement closes and reporting rent can accelerate it.

Is 650 FICO the same as 650 VantageScore? Not exactly. The two models weight your data differently, so you may see a small gap between them — but both classify 650 as fair, so the practical takeaway is the same regardless of which one a lender pulls.

Can I be denied with a 650 even though I'm above the minimum? Yes — and this surprises people. The score gets you in the door, but lenders also weigh your debt-to-income ratio, the age and depth of your credit file, your credit mix, recent inquiries, and your income stability. A thin or young file, a high DTI, or a burst of recent applications can lead to a denial even at 650, while a deep file with low DTI can get a borderline score approved. Build the whole profile, not just the number.

What's the fastest single thing I can do to raise a 650? Lower your credit utilization. With the average 650 borrower at nearly 48% utilization, paying balances down before the statement closing date is the highest-impact move you can make in the shortest time.

Will reporting my rent actually help at 650? Yes — rent reporting is especially effective for fair and thin-file profiles. TransUnion found an average lift of nearly 60 points when rental payments were added, and back-reporting up to 24 months of history can compound that effect.

Disclaimer: Nothing in this article constitutes a guarantee of credit improvement. Every individual's financial situation is different, and the strategies, techniques, or examples discussed may not apply to everyone. Arcane Credit does not guarantee any increase in your credit score. Results may vary and can be influenced by multiple factors, including your activity with other creditors. Arcane Credit does not remove accurate negative information from credit reports.

Written by Hichem Hannafi, Co-Founder, Arcane Credit