My Journey: From Zero to 805 Credit Score in 8 Months.

I moved to the U.S. with no credit history and reached an 805 score in 8 months. Here is the exact, documented strategy I used—from rent and bill reporting to utilization optimization—to build my credit.

When I moved to the United States a few years ago, I had no credit score. No credit history. Not a single tradeline on file. I was what's known as "credit invisible."

I quickly realized how costly that can be.

It's not just about mortgages and credit cards. Landlords check your credit before approving a lease. Mobile carriers review it before setting up a plan. Auto insurers use it to determine your rates. Some employers even consider it during the hiring process.

Without credit in the U.S., you either pay more for everything—or you don't get approved at all.

Even small differences in your credit score can translate into thousands—sometimes tens of thousands of dollars over your lifetime.

Consider this: the average 30-year mortgage is around $400,000. Someone with a 760+ credit score might secure a rate near 6.5%, while someone with a 620 score could be offered closer to 8% on the same loan.

That difference adds up to roughly $425,000 in additional interest over the life of the loan—for the exact same property.

The same principle applies to auto loans, personal loans, and credit cards. According to Experian's 2024 data, the average U.S. credit score is about 715, which means many people are leaving significant money on the table simply because they were never taught how the system works.

So I decided to understand how credit scoring actually works, build a strategy around the underlying mechanics, and execute it consistently.

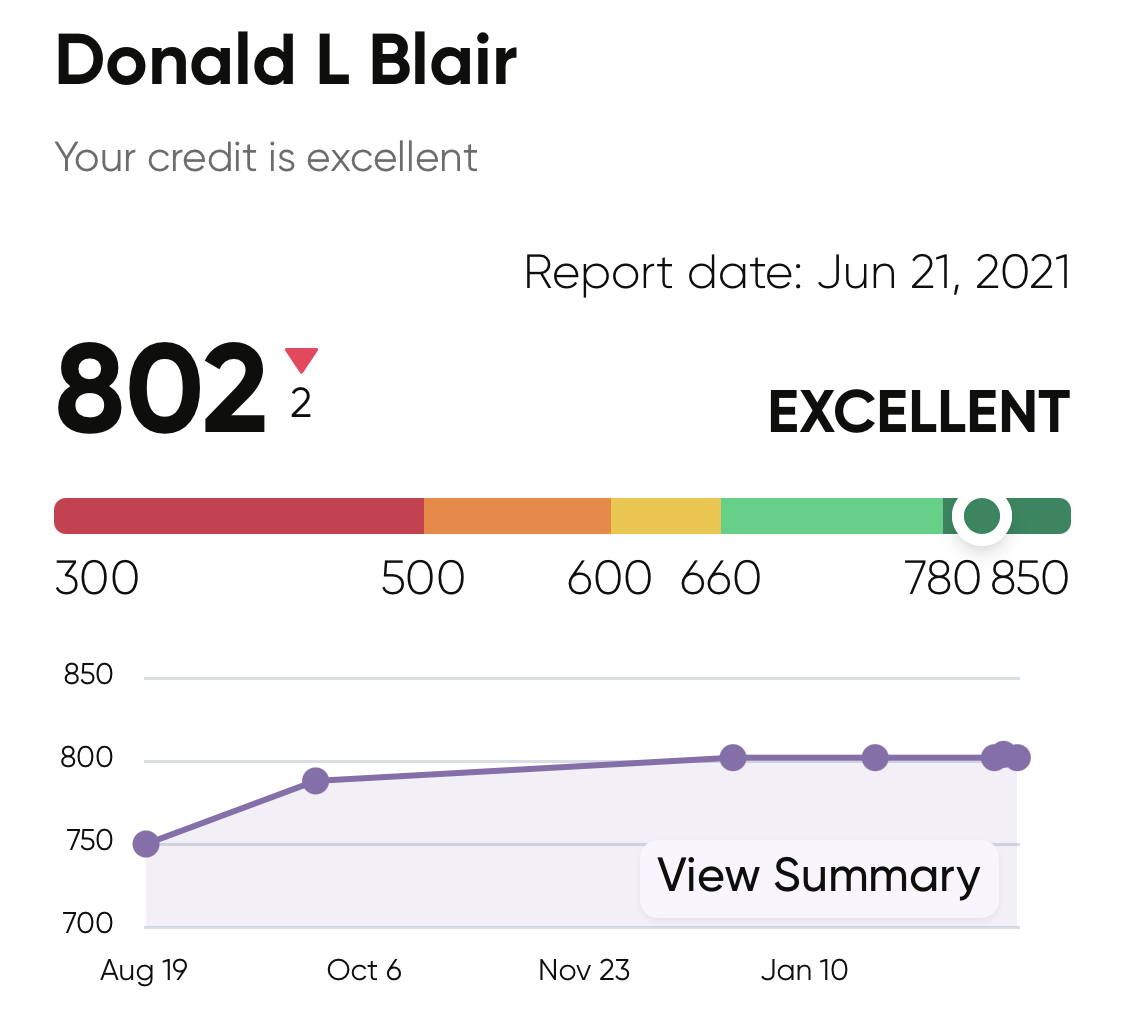

Eight months later, my score reached 805.

I secured my first car with a 0.99% APR. I was approved for a home in one of the most desirable suburbs in Las Vegas. My credit card limits exceeded $20,000, and I began earning a few hundred dollars per month in cashback.

All in under a year.

The good news is that the rules are not particularly complex. Once you understand them, you can use them to your advantage.

How Credit Scoring Actually Works

There are two major scoring models you need to know: FICO and VantageScore.

FICO is used by 90% of top US lenders, including nearly every mortgage and auto lender. VantageScore is used by most credit monitoring apps and is growing fast with lenders too.

The exact formulas are trade secrets. But the factors they weigh are public.

FICO Score Breakdown:

- Payment History — 35%

- Credit Utilization — 30%

- Length of Credit History — 15%

- Credit Mix — 10%

- New Credit — 10%

Source: myFICO — What's in Your Credit Score

VantageScore 3.0/4.0 Breakdown:

- Total credit usage & available credit — ~30%

- Credit mix & experience — ~21%

- Payment history — ~20%

- Age of credit history — ~11%

- New accounts — ~5%

Source: VantageScore — Credit Scoring 101

As you may have noticed, Two of the five factors (utilization + payment history) account for 65% of your FICO score, and roughly 50% of your VantageScore. If you only focus on those two, you're already ahead of almost everyone else.

Here's a closer look at each factor, starting with the most misunderstood:

1. Credit Utilization

This is one of the most misunderstood parts of credit scoring. The standard advice is to keep your credit utilization under 30%. That number is a bit misleading, especially if your goal is 800+.

A better target is 1–2%, with 10% as an absolute ceiling.

The 30% threshold isn't where utilization starts mattering. It's just the point where damage accelerates. In reality, utilization affects your score on a sliding scale — the lower, the better.

Look at FICO's own guidance: consumers with FICO 8 scores of 800+ have an average utilization of about 7%. The fastest climbers usually keep theirs under 2%.

Having existing credit doesn't mean stopping card usage entirely.

The key detail most people miss: pay your full balance before the statement closes, not by the due date.

This single habit has more impact on your score than almost any other tactic.

Credit card issuers and lenders report your balance to the bureaus at the end of your billing cycle — usually at the end of the month or the first few days of the next. Whatever balance is on file when that snapshot gets sent is what shows up on your credit report.

The bureaus don't know you're about to pay it off. They don't care. They just see the number.

So if you spent $2,000 in October and your statement closes on October 31st with a $2,000 balance, Experian, Equifax, and TransUnion all see: this person used $2,000 of credit. Even if you paid it on November 3rd. Even if your due date is November 25th.

Meanwhile, your utilization ratio spikes, and your score takes a hit.

The approach: pay the full balance on or around the 20th of each month — before the statement closes. Some pay twice a month to be safe.

The result: reported utilization stays at 0–2%, with no impact on rewards earnings.

Credit Limit

There's a second lever most people ignore.

The more credit you have available, the lower your utilization ratio — even if your spending stays the same. Spending $1,000 on a $5,000 limit is 20% utilization. Spending the same $1,000 on a $25,000 limit is 4% utilization.

Same behavior. Totally different score impact.

Request credit limit increases regularly.

Most issuers will raise your limit every 6–12 months if your payment history is clean. You can usually do it in-app with a soft pull that doesn't affect your score. If they won't do it without a hard pull, wait until you're deeper into your credit-building timeline before asking again.

2. Payment History

Payment history is 35% of your FICO score and roughly 20% of your Vantage Score.

Here's the good news: if you're already doing the utilization strategy from section one, you're winning this one automatically. Because you're paying everything in full, before the statement closes, every month.

The cost of a single missed payment is significant.

A single 30-day late payment can drop your score by 50 to 100+ points. According to Experian, late payments stay on your report for seven years.

Late payments remain on your credit report for up to seven years — the impact is long-lasting.

Here's a reliable system for keeping payment history clean:

- Set up autopay for the minimum payment on every account. Treat this as a safety net, not a primary payment method. If you forget, autopay serves as a failsafe against a missed payment.

- Go in manually and pay the full statement balance before the statement closes. This is the move that protects your utilization ratio.

- Set calendar reminders for the 20th of every month. Make it a habit you don't skip.

Autopay alone will protect your payment history. Manual full payments will protect your utilization ratio. Doing both is how you build the profile that gets to 800.

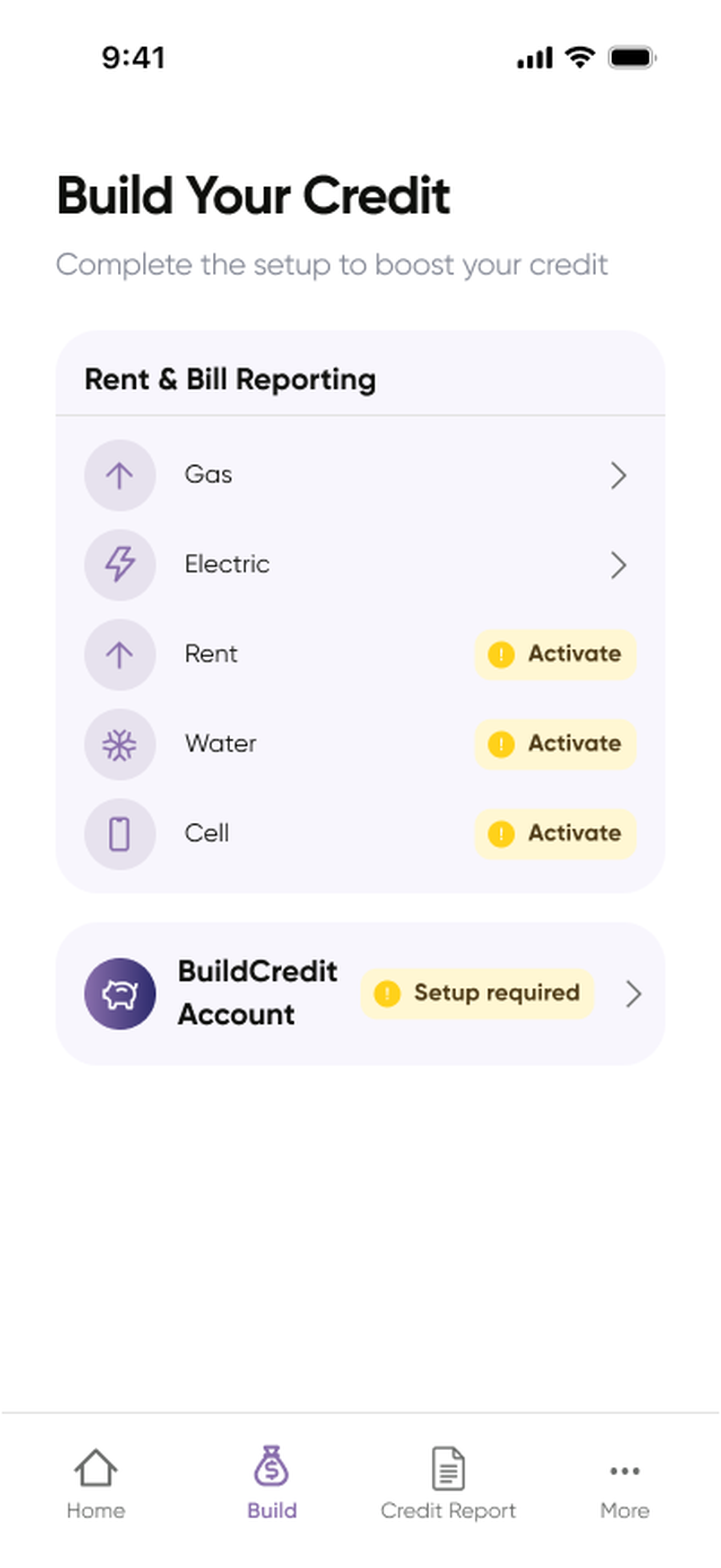

Rent & Bill Reporting

You're probably paying a few thousand dollars a month in rent. Plus electricity, gas, water, and a cell phone bill on top of it.

Those are real, recurring, on-time payments every single month.

Historically, these payments counted for nothing on a credit report.

That's changed.

Rent reporting services such as Arcane Credit now connect directly to your bank account, identify your rent and utility payments, and report them to the bureaus every month — no landlord approval required, no paperwork.

Arcane Credit is built specifically for this. It uses Plaid to link your bank account, automatically identifies your recurring rent and bill payments, and reports them to the credit bureaus month after month. You pay $3.99/mo (billed yearly) or $5.99/mo (billed monthly) and you get a fully hands-off experience after setup, which also includes access to a Credit Builder Loan, 24/7 credit report access, VantageScore® monitoring and real-time credit alerts. There's no hard pull to sign up.

Compare that to the competition:

| Service | Monthly Cost | What Gets Reported |

|---|---|---|

| Arcane Credit | $3.99/mo (yearly) or $5.99/mo | Rent + electric + gas + water + cell phone |

| Self.inc | $6.95/mo | Rent + utility |

| Ava (meetava.com) | ~$10/mo | Rent + utility |

The data here is compelling.

A 2021 TransUnion analysis found that incorporating rental payments into credit reports boosted consumer credit scores by an average of nearly 60 points. And According to VantageScore, consumers who were previously considered "credit invisible" see their average VantageScore 4.0 rise to around 654. Additionally, about 99.7% of these individuals achieve a score of 620 or higher, meeting the minimum requirement for mortgage eligibility under Fannie Mae and Freddie Mac guidelines.

One underused strategy worth highlighting. If you've been paying rent and utilities for years but none of it's ever been reported, you can leverage Arcane Credit's Score Boost to retroactively report up to 24 months of your past payment history to the credit bureaus. It is a one-time $39.99 add-on but it is incredibly powerful and way cheaper than competitors such as self.inc who typically charge at least $49.95 for the same service. Instead of your credit report showing 4 or 5 months of history, the bureaus see two full years of on-time payments — essentially backdated into your file. VantageScore officially states that adding rental data to an established credit file can add up to 150 points to your score.

Source: VantageScore — Positive rent-payment data has powerful credit-score impact

There's almost no other move in credit-building that's this asymmetric. You're not changing your spending, not taking on debt, not opening new accounts. You're just making the work you're already doing visible to the credit bureaus.

3. Credit Mix & Experience

Credit mix doesn't get talked about enough.

FICO gives it 10% of your score. VantageScore weights it even higher — around 21% of the total model (Credit Mix and experience). That's more than payment history in VantageScore.

Source: VantageScore — The Complete Guide to Your VantageScore

The concept is simple. Lenders want to see that you can responsibly handle different types of credit — not just one.

There are two major categories:

- Revolving credit: credit cards, lines of credit

- Installment credit: auto loans, personal loans, student loans, mortgages

Someone who manages both responsibly looks like a safer bet than someone who only has a credit card. The scoring models reward that.

If your only credit account is a credit card (or a few credit cards), you're leaving points on the table.

The Easiest Way to Add an Installment Account

You don't need to take out a car loan or a personal loan just to fix your credit mix. There's a purpose-built product for this situation: a credit-builder account.

Here's how it works:

- You don't receive any money upfront

- You make small monthly payments that get locked into a Certificate of Deposit (CD) Account.

- Those payments get reported to all three bureaus as an installment tradeline

- When the term ends, you get the money back (minus interest and fees)

In other words: you pay yourself to build credit. It's similar to a savings account, but with a credit-reporting side effect.

Arcane Credit's BuildCredit Account is exactly that. It is a Credit Builder Loan that is accessible with every membership. It's issued by Cross River Bank (Member FDIC) through their partner BuildCredit, LLC — so your money is federally insured. Monthly payments report to Equifax, Experian, and TransUnion.

There's a $9 origination fee and a 15.68% APR. It helps to understand what that fee actually covers. You're not taking on real debt. The "interest" is the cost of the credit-building service, and the savings portion comes back to you at the end. For most people, it's a small price for a legitimate installment tradeline reporting to all three bureaus for the full life of the loan.

At $3.99/month, the math is obvious. You're paying less than a cup of coffee. For most people looking to hit 800, this is the single highest-leverage decision in the whole build.

4. New Credit New Credit & Length of Credit History

Opening new credit accounts does two temporary things to your score:

- Adds a hard inquiry to your report

- Lowers your average age of accounts

A hard inquiry typically drops your score by 5 points or less, according to Experian. It stays on your report for two years but usually only affects your score for about 12 months.

The drop from opening a new account is usually similar. A few points. Short-lived. Recoverable.

Opening multiple accounts in a short window compounds the impact — each inquiry signals elevated borrowing risk. The recommended approach: open only the accounts needed, and ideally at the same time, so the temporary score dip consolidates into a single recovery. For those planning a mortgage application, avoid new credit for at least a full year beforehand. Here are the accounts worth opening during the credit-building phase: avoid new credit applications at least full year before applying.

Secured Credit Cards

A secured card requires a refundable deposit, which becomes your credit limit. It's the entry point when most unsecured cards won't touch you.

Two strong options: the OpenSky Secured Visa and the Self.inc Secured Visa. Neither requires a credit check. They can be opened individually or together. self.inc. Both are great options and it's absolutely fine to either combine them or to open either. They both don't require a credit check to apply. After 6 months of on-time payments, OpenSky automatically evaluates you for their Gold unsecured card. No reapplication, no extra credit pull.

Source: OpenSky — How to Graduate to an Unsecured Credit Card

Deposit strategy: the higher you can afford the better. Remember, a higher credit limit helps you maintain a lower credit utilization ratio especially, you just need to ensure you're not overusing it and stay within the advisable 1-2% credit utilization we discussed above.

Ava A newer entrant with an interesting angle. They offer an unsecured card with no credit history required — almost nobody else does this. As of today, they report a $2,500 credit limit to the bureaus but cap your actual spending at $25/month (enough for one subscription like Netflix or Spotify). So your utilization is permanently locked at about 1%, automatically.

The model is particularly well-suited to those who want automatic utilization control without the risk of overspending.

Arcane Credit Account

The day you open your secured card account(s), sign up for Arcane Credit. For $3.99/month on the yearly plan, you will get:

- Rent reporting, up to 24 months back-reported with Score Boost.

- Electric, gas, water, and

- cell phone reporting

- 24/7 credit report and score access

- Real-time credit alerts

- BuildCredit Account access, the installment tradeline reported to all 3 bureaus that we discussed above

The reason to do this day one is leverage. Your first secured card is going to report a single revolving tradeline with a small limit. On its own, it builds credit slowly. Stacking rent, utilities, and a credit-builder installment account on top of it accelerates the timeline dramatically.

That's the complete setup. Less is more in credit-building. From here, execution is everything: full payments every month, consistent habits, no shortcuts. Follow the strategy consistently and reaching your credit goals within a year is a realistic outcome.

Quick disclaimer: Results vary based on starting point, income stability, and consistency with the strategy above.

For those starting from zero with no negative history, this timeline is faster than most approaches available — and the strategy is fully repeatable.

The Mistakes That Quietly Tank Your Progress

These are the most common mistakes that quietly stall credit progress:

- Carrying a balance to "build credit". This is the most common myth in personal finance. As discussed earlier in this article, you do not need to carry a balance or pay interest to build credit. Paying the statement balance in full every month builds credit just as effectively — and costs you zero in interest. Experian confirms this.

- Waiting until the due date to pay Your due date and your statement closing date are different. The balance on your statement close date is what gets reported. If you wait until the due date, you've already reported high utilization — even if you then pay it off. Pay before the statement closes, not before it's due.

- Not reporting your rent and utilities You're already making these payments. If they're not being reported, you're leaving free credit-building on the table every single month. This is the single easiest mistake to fix.

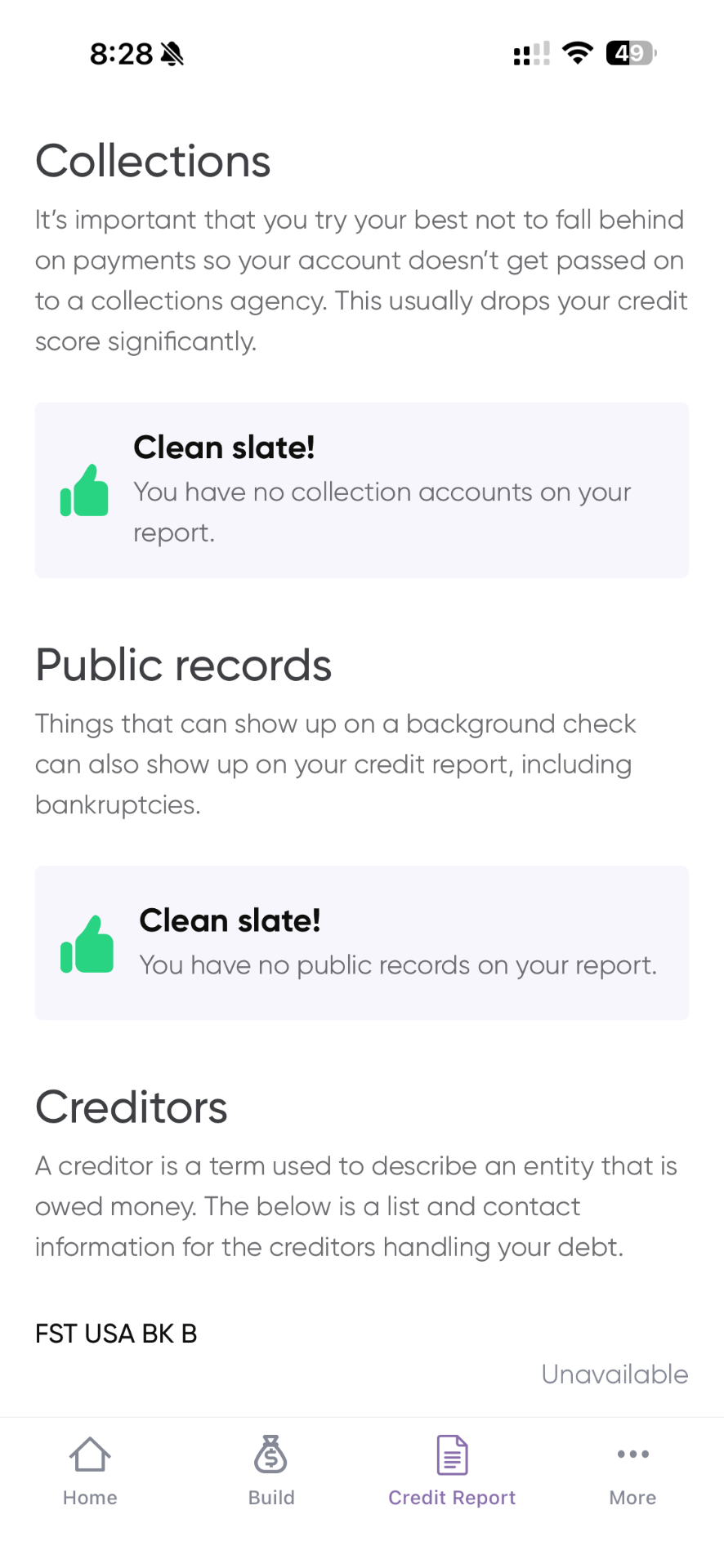

- Closing accounts. When you close an account, two bad things happen. You lose that credit limit (which increases your utilization ratio across your remaining cards). You also eventually lose the account's age from your average account age calculation which affects your length/age of your credit history which accounts for roughly 15% of your credit score. Keep old accounts open, even if you don't actively use them, keep them active.

Checking your score only after something bad happens: Arcane Credit gives you 24/7 access to your VantageScore and full report. Monitor it regularly. Early detection of errors or fraud can save your score. According to a Consumer Reports investigation, more than 34% of people found at least one error on their credit report. Dispute errors immediately through Experian, Equifax, or TransUnion directly. A single error removed can be worth 20+ points.

Conclusion

Here's the whole strategy in five lines:

- Keep utilization at 1–2% — pay before the statement closes, not before the due date.

- Never miss a payment — set up autopay as a backup for every account.

- Report your rent and utilities — you're already paying them, make them count.

- Open a credit-builder account — adds the installment tradeline you need for mix.

- Apply for a secured credit card as early as possible, and deposit the highest amount you can comfortably afford.

- Stay patient and monitor your credit regularly.

Disclaimer: Nothing in this article constitutes a guarantee of credit improvement. Every individual's financial situation is different, and the strategies, techniques, or examples discussed may not apply to everyone. Arcane Credit does not guarantee any increase in your credit score. Results may vary and can be influenced by multiple factors, including your activity with other creditors. Arcane Credit does not remove accurate negative information from credit reports.

FAQs

Does checking my own credit score hurt it? No. Checking your own score is a soft inquiry. Soft inquiries have zero effect on your score. Hard inquiries only happen when a lender pulls your credit during an application. You can check your score as often as you want with no consequence.

Do I need to carry a balance on my credit card to build credit? No. This is one of the most persistent credit myths. Paying your balance in full every month builds credit just as well as carrying a balance — and saves you the interest. There's no hidden advantage to carrying debt.

What's the single fastest thing I can do to raise my score right now? Pay down your existing credit card debt to lower utilization. That's the fastest lever you can pull.

Disclaimer:

Nothing in this article constitutes a guarantee of credit improvement. Every individual's financial situation is different, and the strategies, techniques, or examples discussed may not apply to everyone. Arcane Credit does not guarantee any increase in your credit score. Results may vary and can be influenced by multiple factors, including your activity with other creditors. Arcane Credit does not remove accurate negative information from credit reports.

Will rent reporting actually move my score?

A 2021 TransUnion analysis found that incorporating rental payments into credit reports boosted consumer credit scores by an average of nearly 60 points. For people with no credit score at all, it helped them become scoreable. The effect could be bigger for thin-file consumers but still meaningful for established files.

Disclaimer:

Nothing in this article constitutes a guarantee of credit improvement. Every individual's financial situation is different, and the strategies, techniques, or examples discussed may not apply to everyone. Arcane Credit does not guarantee any increase in your credit score. Results may vary and can be influenced by multiple factors, including your activity with other creditors. Arcane Credit does not remove accurate negative information from credit reports.

Is 800 actually necessary, or can I aim lower?

In practical terms, most top-tier rates on mortgages, auto loans, and credit cards start around 740–760. 800+ puts you in FICO's "exceptional" tier and gives you maximum negotiating leverage. Going from 800 to 840 makes little to no difference. But going from 720 to 800 can be worth thousands in lifetime interest savings.

What's the difference between FICO and VantageScore?

FICO is used by most lenders for actual lending decisions (especially mortgages). VantageScore is common on credit monitoring apps and is increasingly used for lending too. The two scores weight factors slightly differently, so you may see a small gap between them — this is normal. Focus on building good habits and both scores will rise together.

How often should I request a credit limit increase?

As often as your credit card issuer allows it. Most major issuers let you request it in-app with a soft pull (no score impact). If an issuer only does hard pulls for limit increases, skip them until you're in a growth phase where one extra inquiry won't matter.

Co-Founder of Arcane Credit. Writes about credit building, consumer finance, and what actually moves a VantageScore.